For many it was a hot August. Time to slowdown, go on holiday, and not worry about financial markets. Of course, there is a lot to worry about, but August performance across most asset classes showed general range-bound behavior with a continued reach for yield within the equity and fixed income asset classes. The tight range was linked to no substantive news to change expectations. After weeks of hype, the comments of Fed Chairman Yellen at the Jackson Hole conference did not serve up anything new. The data driven Fed may raise rates or not based on further confirmation of data that seems stuck in a range.

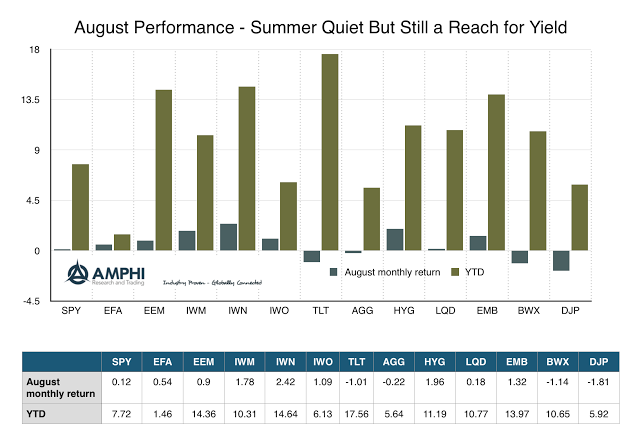

The big winners by ETF performance for the month were the Russell 2000 small cap and value indices as measured (IWM and IWN) and the high yield and emerging market bond indices (HYG and EMB). The S&P 500 index (SPY) gained only 12 bps and the long bond (TLT) sold-off by one percent with choppy performance. August was a difficult month for any active trader given no strong trends.

The economic news only provided further evidence of growth that followed the shallow trends that have been a hallmark for 2016. Growth is nothing like the pre-Crisis period, but rather a muddle that could easily stall or move higher. Inflation is closing in on the Fed 2% target, but ever so slowly. The PCE core is at 1.6% and the CPI ex-food and energy is at 2.2%. There is no evidence of an inflation overshoot and with the rest of world seeing low inflation, these numbers can easily move lower.

As an economist knows, the marginal utility of the next dollar consumed is less valuable then the last. So is it also with monetary policy. Central bankers continue to push on a their money string only to see limited impact. While there may be a growing consensus for fiscal stimulus, there is little evidence that policies are changing radically.

For investor, the fall season starts the day after Labor Day. An election, more talk of Fed action, and markets focusing on growth may change this range-bound behavior and end of the dog days of summer; however, without a market shock there is little that may change expectations.