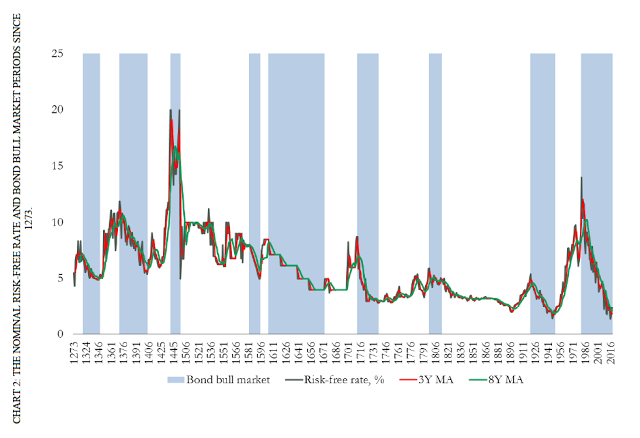

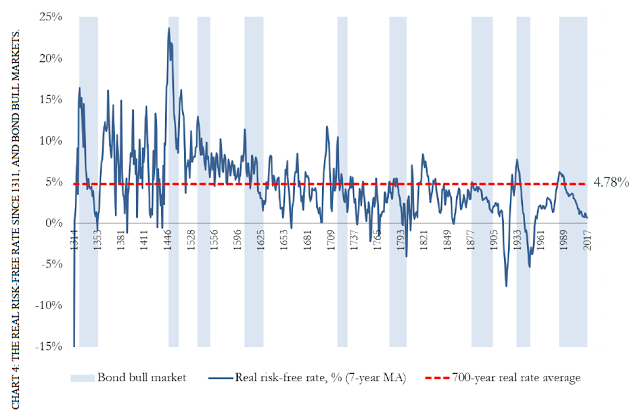

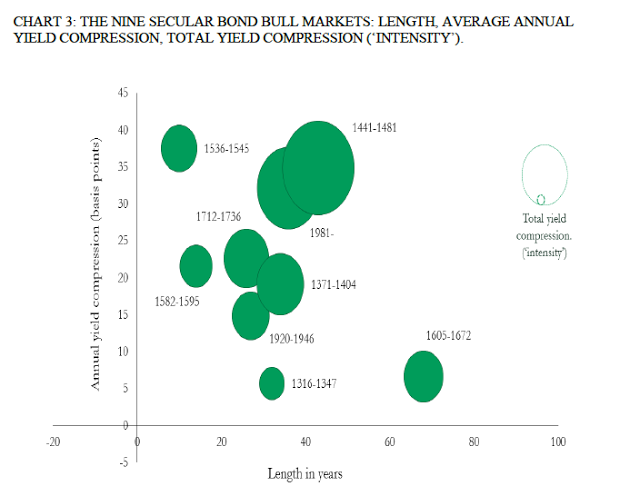

The Bank of England research piece, Eight centuries of the risk-free rate: bond market reversals from the Venetians to the ‘VaR shock’ by Paul Schmelzing, is important reading for any investor. It places the current bond rally which has been going on for over three decades in the long term context of the last 700 years. This bond bull movement is exceptional but not yet extraordinary when look at through history. Unfortunately, all bond rallies will end, but the reasons for ending may vary.

This Bank of England research suggests that bond bears are not just correlated to fundamentals like higher inflation but also underperformance in GDP and equity returns during the 20th century. The author conducts case studies for some of the most recent large bond bear markets in the post-WWII period. He finds that while fundamentals like inflation are a key reason for a bond bear market as in the case of the ’65-’70 sell-off, there have been other cases which are not related to fundamentals like the ’94 bond massacre or the ’03 Japanese VaR shock. The author suggests that central miscommunication or non-fundamentals can also trigger a bond bear market.

Inflation does not currently seem to be a potential driver for a bond bear market, although the author believes that the ’65-’70 fundamental (inflation) reversal may be a likely scenario. Bond bull market trends may last longer than what many expect, but divergences will occur and the reasons may be unexpected.