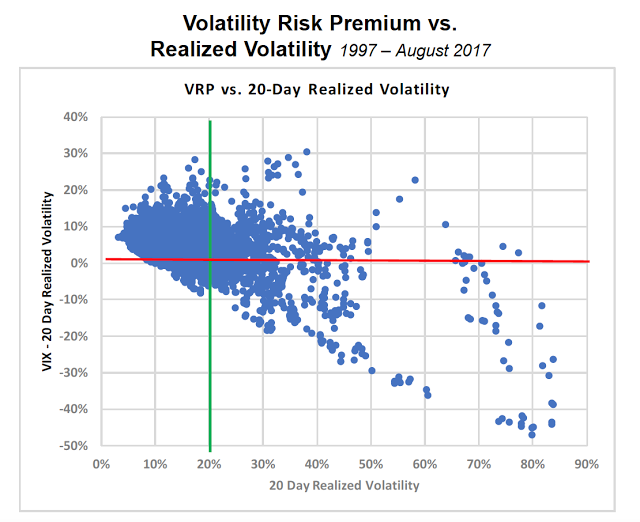

Implied volatility is usually higher than realized volatility so there is a positive volatility risk premium, except when there is a crisis or volatility spike at which time the volatility premium turns negative. A recent CBOE seminar presented a chart on the volatility premium to illustrate the risk.

The numbers suggest that being short volatility gave you a positive premium in a stable world, but when the world is less stable, (higher realized volatility), you do not want to be a vol seller. The chart suggests that there can still be a positive risk premium when realized volatility is high, but the odds work against you. It is a way to get to a realized volatility of more than 20% at current levels, but that world can become a reality quickly if there is an equity sell-off.

It is important to measure your short volatility where you may have been picking up vol premium. If you have too much, now is the time to cut that exposure.