Commodity index investing has not been very successful for investors as measured by leading index total returns since the Great Financial Crisis. The end of the super-cycle has been tough on most investors and only recently has there been a period of extended positive returns based on the rise in oil prices. Is there any relief for investors?

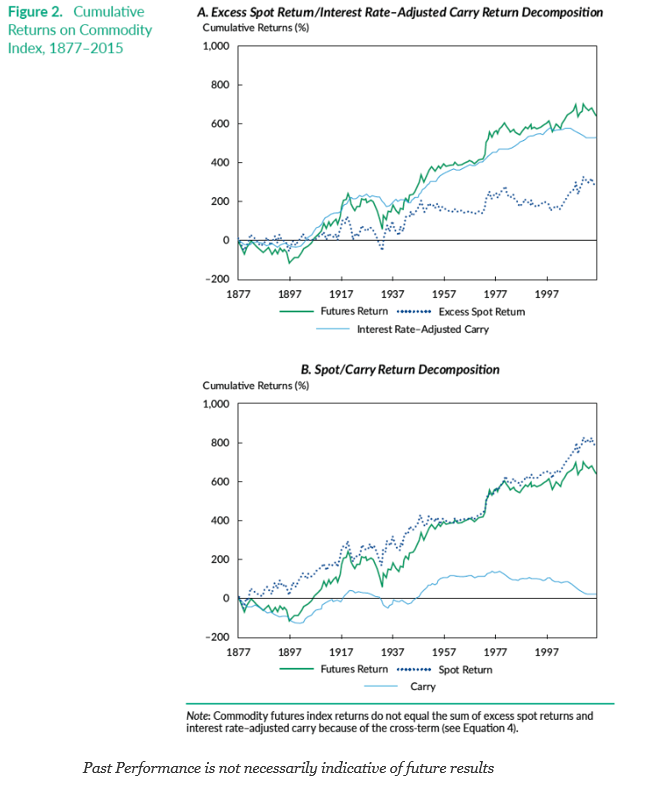

A look at long-term returns for commodity futures suggests that this period is not representative of what may happen in long run; however, long periods of negative performance are not unusual. The recent paper, “Commodities in the Long Run”, published in the Financial Analysts Journal studies commodities since almost the beginning of the Chicago Board of Trade, a period of 140 years. It finds that commodity futures indices have been significantly positive over the large time period, albeit with high volatility.

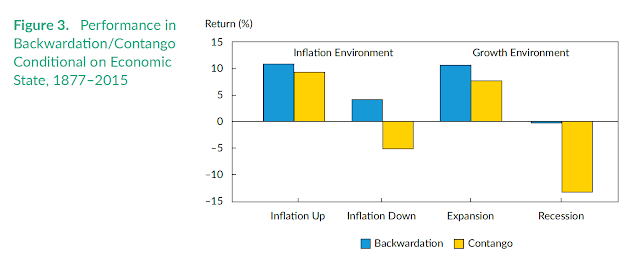

The work also shows that the key driver of commodity futures returns are the interest rate adjusted carry and not the spot price. Backwadation and contango do matter and this carry effect is different than the movement in short-term interest rates. Backwardation is a strong positive condition for commodity returns. Additionally, performance will differ on the macroeconomic conditions with high inflation and growth being two states that positively impact return performance. Notably, in an inflation up and expansion period commodity returns are positive regardless of the backwardation or contango.

Commodities will add value as a diversifier to a portfolio especially during certain economic states like higher inflation. Given the low correlation to stocks and bonds, volatility will be lowered with even a small allocation to commodities and there will be an increase in Sharpe ratio. The benefits from commodities can be achieved either through a long position or a long-short position through backwardation and contango.

Our view is that commodities should be incorporated as a core allocation for a well-diversified portfolio but this allocation should be dynamic. Periods of sharp economic downturn should call for lower allocations or exposure through long-short carry positions. More importantly, asset allocation decisions should not be skewed by the recent post financial crisis return performance but should be based on a longer-term view consistent with the data.