Gold is hard to understand as an investment. Sometimes it behaves like an inflation hedge but at other times it does not. Sometimes it responds to the real cost of funds, and sometime it does not. It can serve as a safe asset, yet it has sold-off in a crisis. It can be the uncorrelated asset of frustration, but a longer examination tells us about investment deep investor expectations. Gold, over the last decade, can be viewed through three major themes.

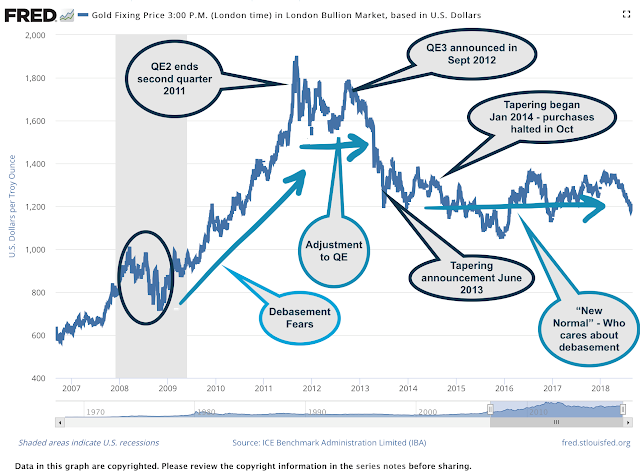

- The debasement fears period – This was the period of maximum gain in quantitative easing. This period ends with QE2 and when QE policy seemed to be a limited accelerant to the real economy.

- The adjustment to QE period – Contrary to many analysts the exposure of the Fed balance sheet did not led to a surge in inflation. In fact, large central bank balance sheets did not even allow inflation to get to target levels. Even with negative rates on trillions in bonds, investors did not view gold as essential if there was not going to be a debasement of nominal assets.

- The “who cares about debasement” or “new normal” period – The third period began with the tapering and moved to the new period of Fed adjustment with increasing rates. Inflation is closer to target, but the expectation of a monetary debasement of bonds has left investors to be replace by a sense of complacency or normalcy. Investors have found a new equilibrium where they believe central banks will not drive the economy to the monetary brink. Balance sheet holdings will be higher than pre-crisis levels, but the potential for a significant inflation overshoot is minimal. Financial assets have exploded to the upside, but gold has still doubled since 2007 levels.

The question is whether there will be a new fourth period for gold and what will it look like. We may not know what this new gold environment will look like until central banks are forced to again change policy.