An ensemble approach to modeling can be an effective way to get a good idea of the consensus and differences in forecasts on futures moves in the Fed funds. This is an effective alternative to looking at Fed funds futures and options as a market estimate.

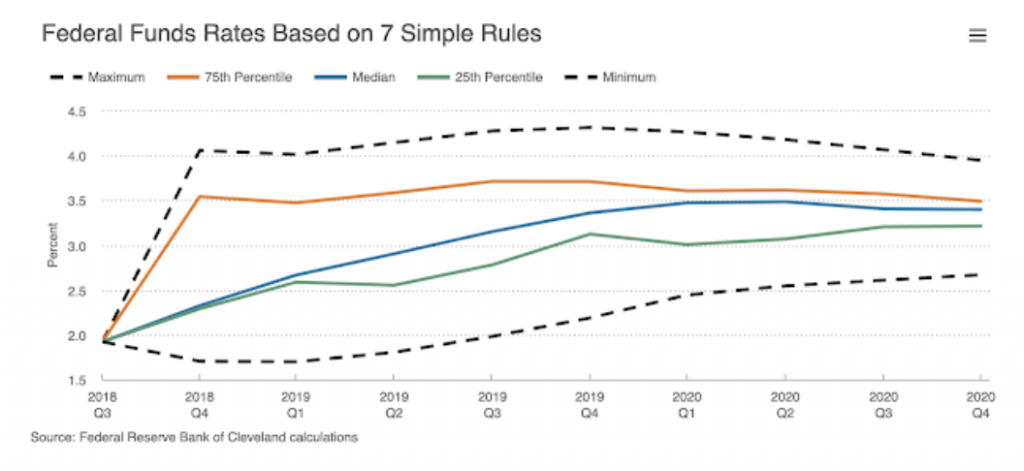

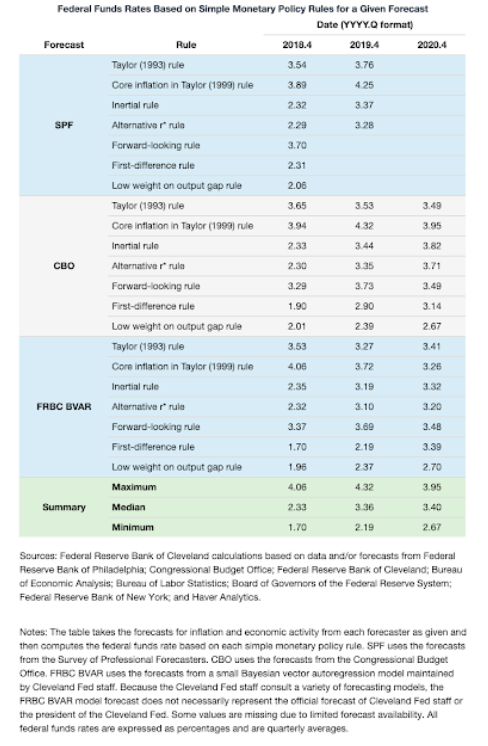

A nice place to show the impact of ensemble modeling is the Cleveland Fed research site which provides quarterly updates of Fed fund forecasts using seven different models. The next update is at the end of this month. The ensemble is developed through using some variations on Taylor Rules that are relatively easy to estimate and have done a good job in the past.

The approach is simple. The different forecast models are employed with different forecast assumptions. A nice benefit of this approach is that anyone’s forecasts can be used with the same set of models as a comparison. It is not the underlying assumptions that are compared but the forecast output through these standardized sets of models. While the Cleveland Fed updates this approach on a quarterly basis, model forecasts against current expectations can be done at anytime. You can call the differences model dispersion or uncertainty. All of these models have rational intuition, so the dispersion across models tells us something about underlying economic uncertainty.

By comparison to the last Cleveland estimates before year-end, we are in a new monetary world. 2018 is ancient history. We are currently between the 25 percentile and minimum forecast. Trading that range is the place of global macro opportunity. Currently, the entire range of forecasts will be lower and likely tighter.