There should be concerns about the amount of corporate leverage in the economy, but if there is no catalyst credit event, current risk is limited. We are not downplaying potential credit risk, but there needs to be focus on the right issues that will drive corporate bonds spreads higher.

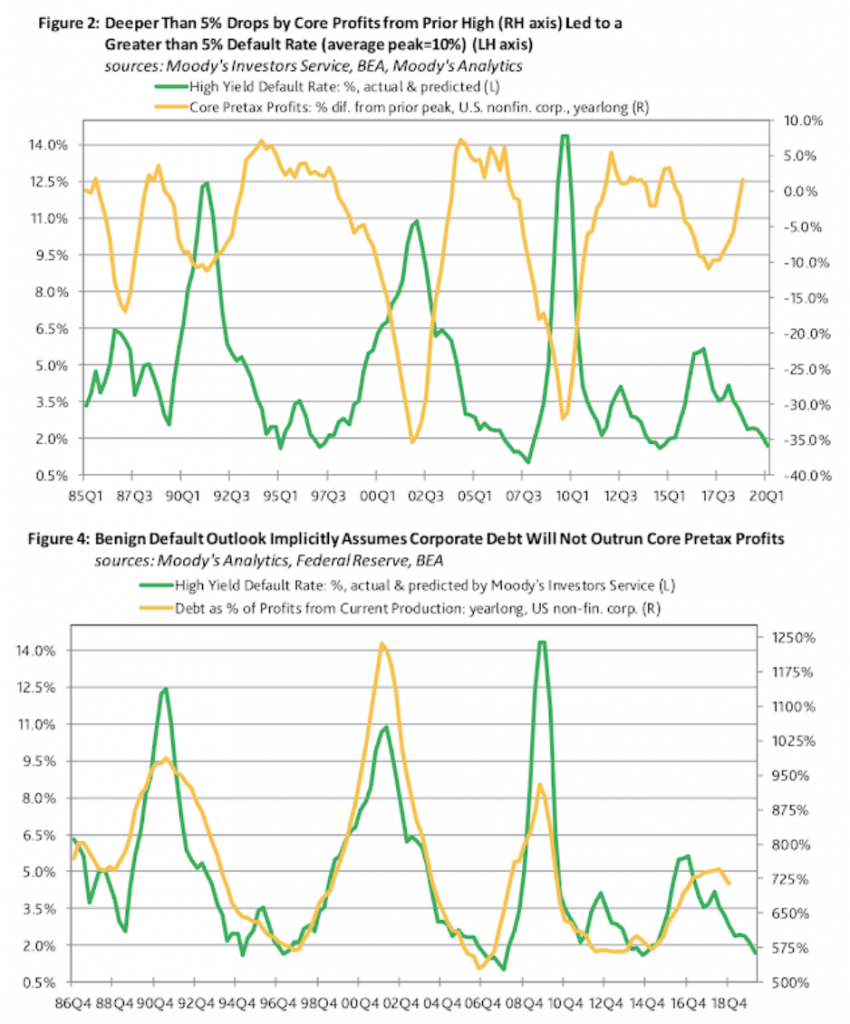

If corporate profits fall, there will be an increase in the high yield default rate. Follow the profits, and with profits moving higher, default rates have fallen. See Moody’s Analytics, “Benign Default Outlook Implies Profits Will Outrun Corporate Debt”. If the profit environment changes, credit risks will respond.

Debt as a percentage of profits is more important than debt as a percentage of GDP. The size of the debt to GDP may not forecast defaults but it does tell us the potential for severity if there is a profit decline. Consequently, following forward guidance on earnings may give an early signal on potential default and widening of spreads. Currently, earnings guidance has turned negative, yet we are seeing that earnings have been more robust than forecast last quarter. For the first quarter, approximately 2/3rds of companies reported earnings or a revenue surprise. Nevertheless, earnings guidance has turned negative for the first time in two years. This suggests that we may be on the cusp for changes in spreads.