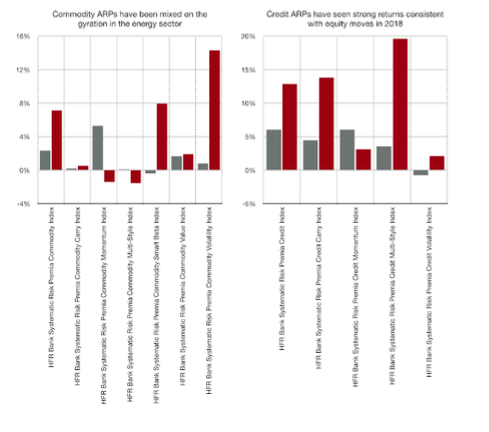

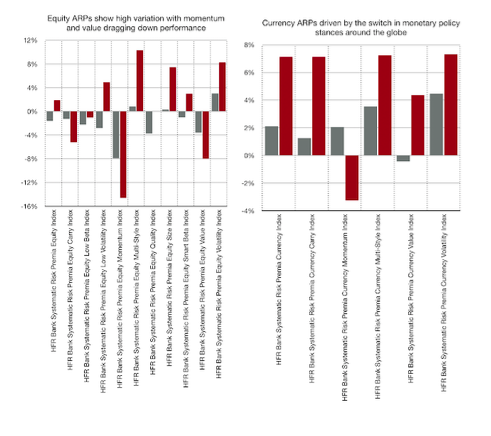

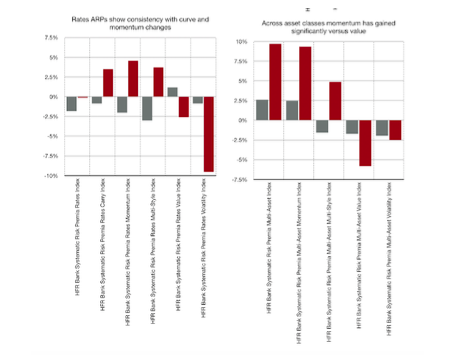

A comparison of ARPs across asset classes and styles from the HFR indices shows consistency with the macro environment. We equalized the HFR ARP indices to a ten percent volatility for ease of discussion. April monthly returns are in grey while year to date returns are in red. The returns were generally lower than the market exposures, which were expected. The HFR numbers are averages and have shown significant dispersion. The low correlation across ARPs will create opportunities to improve the return to risk ratios through portfolio blending.

Commodity ARP returns were mixed given the curve fluctuations in the energy sector; however, the long-only smart beta index generated strong returns. The credit ARP sector also was a strong gainer based on the tightening of spreads in tandem with the gains in equity since the beginning of the year. Credit spreads will often proxy for movements in the equity markets; however, equity ARPs were mixed. While some equity strategies like volatility showed strong gains, core strategies such as momentum and value generated marginal returns for this year. With the strong gains across all equity markets, the short sides of ARP trades have been a significant drag on performance. The losers of the fourth quarter were the strongest winners in 2019. Currency ARPs were strong performers based on the changes in the liquidity stance of global central banks. These returns are somewhat high given the absolute movement in currency rates. Rates ARPs were consistent with the momentum moves across the globe as well as recent movements in yield curve. The bundled ARP returns especially in momentum across all asset classes have shown significant through this year.